Inside Deep Tech Market: What the Data Tells Us In 2026

Inside Deep Tech Market: What the Data Tells Us In 2026

Recently, Celesta Capital Founding Managing Partners Nic Brathwaite and Michael Marks took the stage at Deep Tech Week NYC for a panel event conversation on the state of deep tech investing. The event brought together founders, LPs, and investors for an afternoon focused on where the deep tech market stands today and where it is heading.

The discussion, led by Partner David Goldman, covered a wide range of ground: how deep tech has evolved from a niche category into a major share of global venture funding, the shifting economics between software and hardware, exit dynamics in semiconductors, the rise of defense tech, and practical fundraising advice for founders navigating this market. Below, we walk through some key insights shared during the conversation.

Recently, Celesta Capital Founding Managing Partners Nic Brathwaite and Michael Marks took the stage at Deep Tech Week NYC for a panel event conversation on the state of deep tech investing. The event brought together founders, LPs, and investors for an afternoon focused on where the deep tech market stands today and where it is heading.

The discussion, led by Partner David Goldman, covered a wide range of ground: how deep tech has evolved from a niche category into a major share of global venture funding, the shifting economics between software and hardware, exit dynamics in semiconductors, the rise of defense tech, and practical fundraising advice for founders navigating this market. Below, we walk through some key insights shared during the conversation.

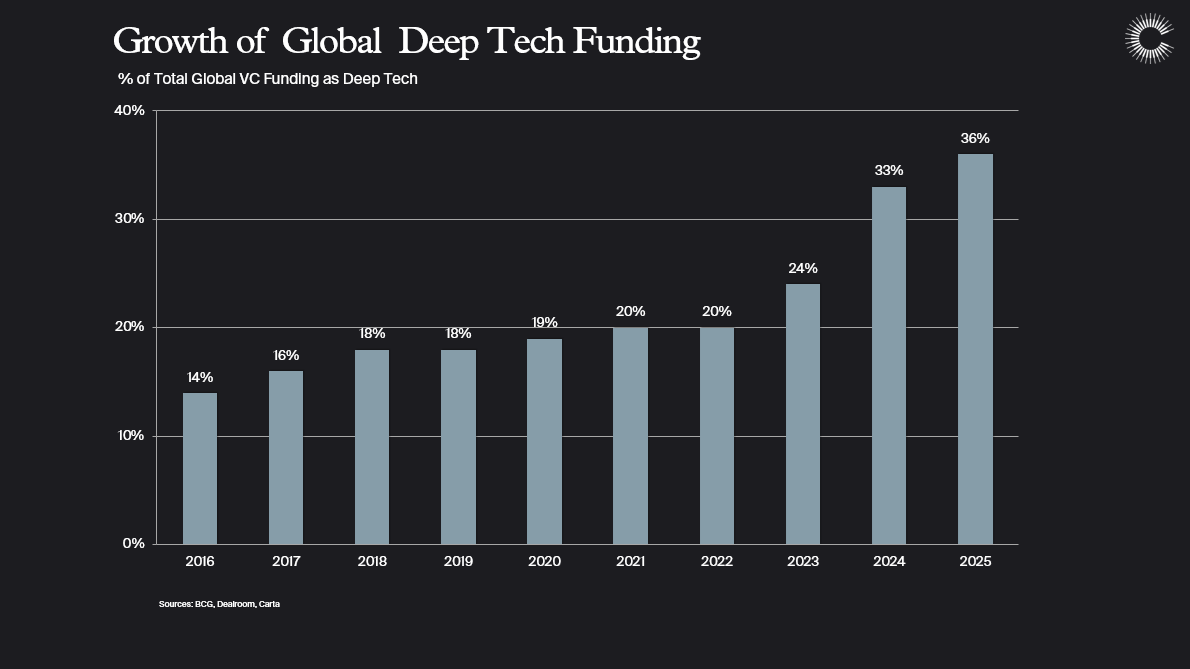

Deep Tech Funding Has More Than Doubled as a Share of Global VC

Deep tech now accounts for 36% of total global VC funding, up nearly 3x since 2016. That growth has been steady, but the pace accelerated meaningfully after 2022, coinciding with the release of ChatGPT and the skyrocketing demand for improved performance across all categories of AI infrastructure.

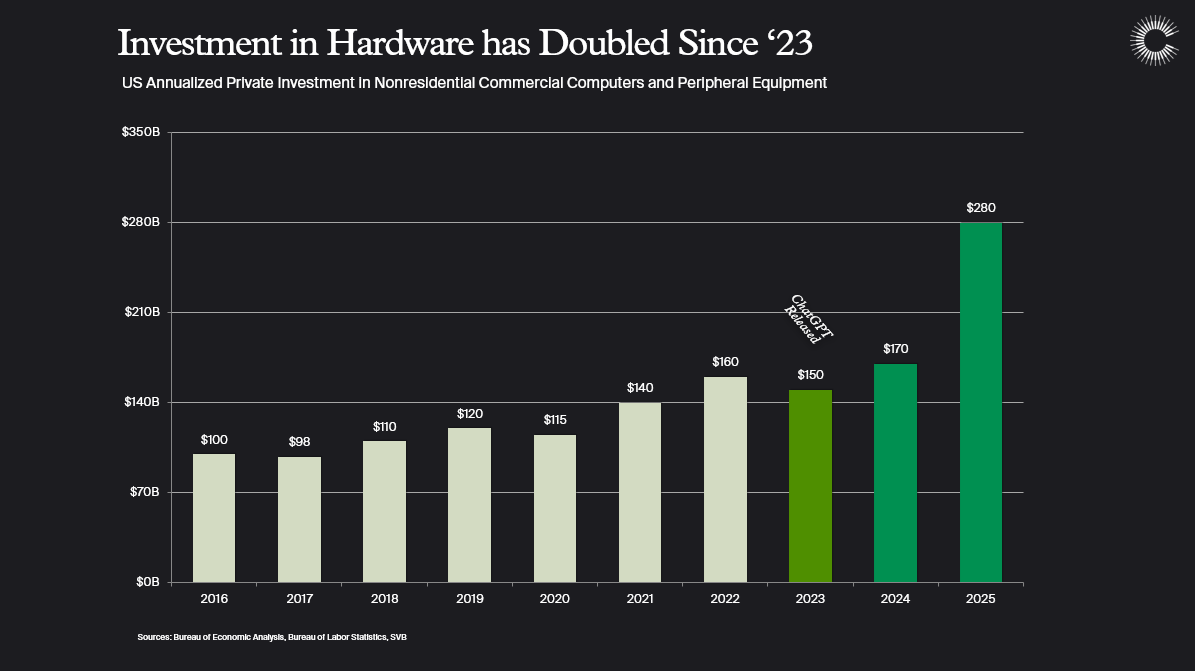

Bearing out that story, U.S. private investment in computing equipment has roughly doubled since 2023, reaching $280 billion on an annualized basis in 2025. This is not just a software-driven cycle. Capital is flowing into physical infrastructure at relative rates not seen in decades.

For Celesta, which has been investing in hardware and deep tech since 2013, this shift validates a thesis that long predates the current AI wave. As Nic Brathwaite put it during the panel: “The challenge now is not finding investors interested in the category but maintaining discipline as more capital floods in.”

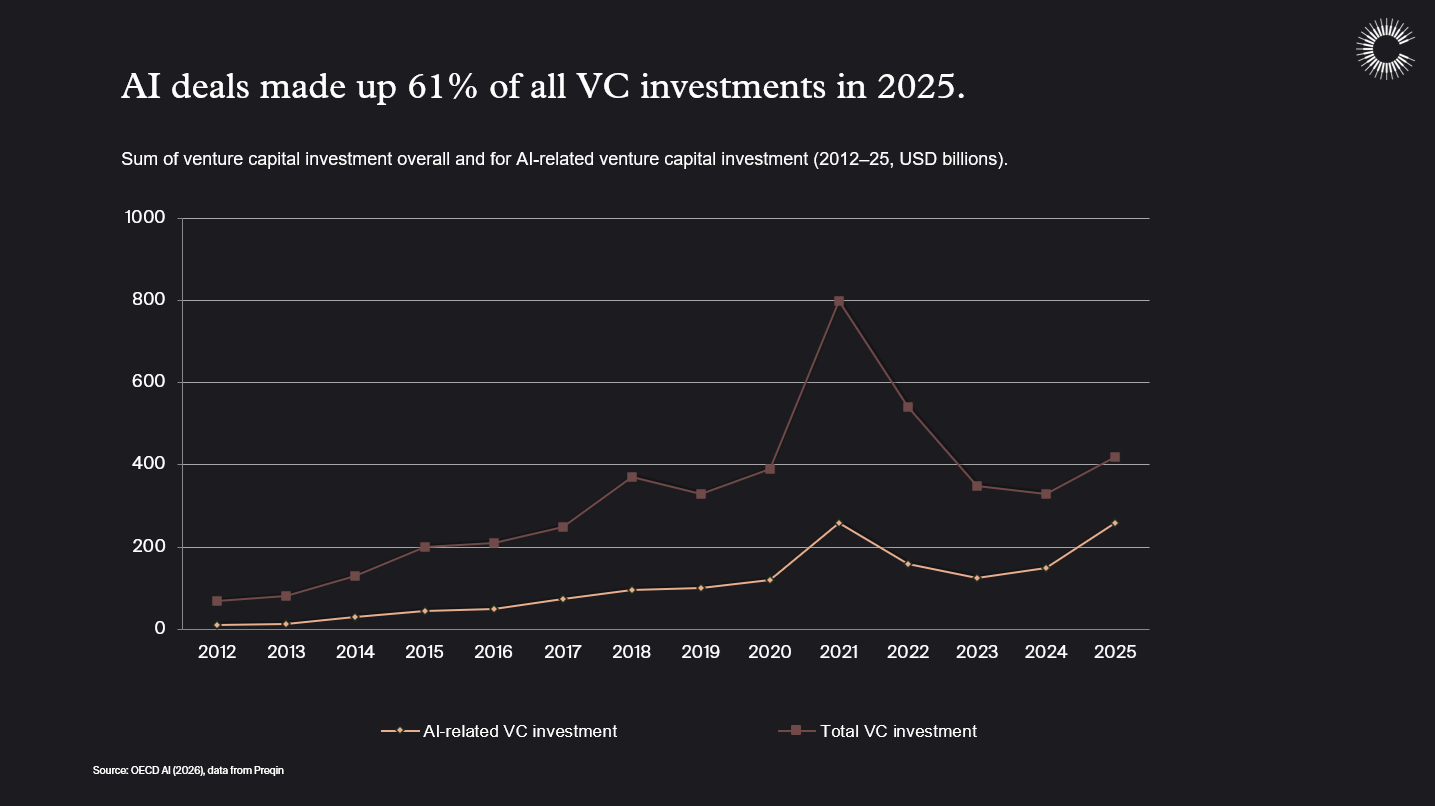

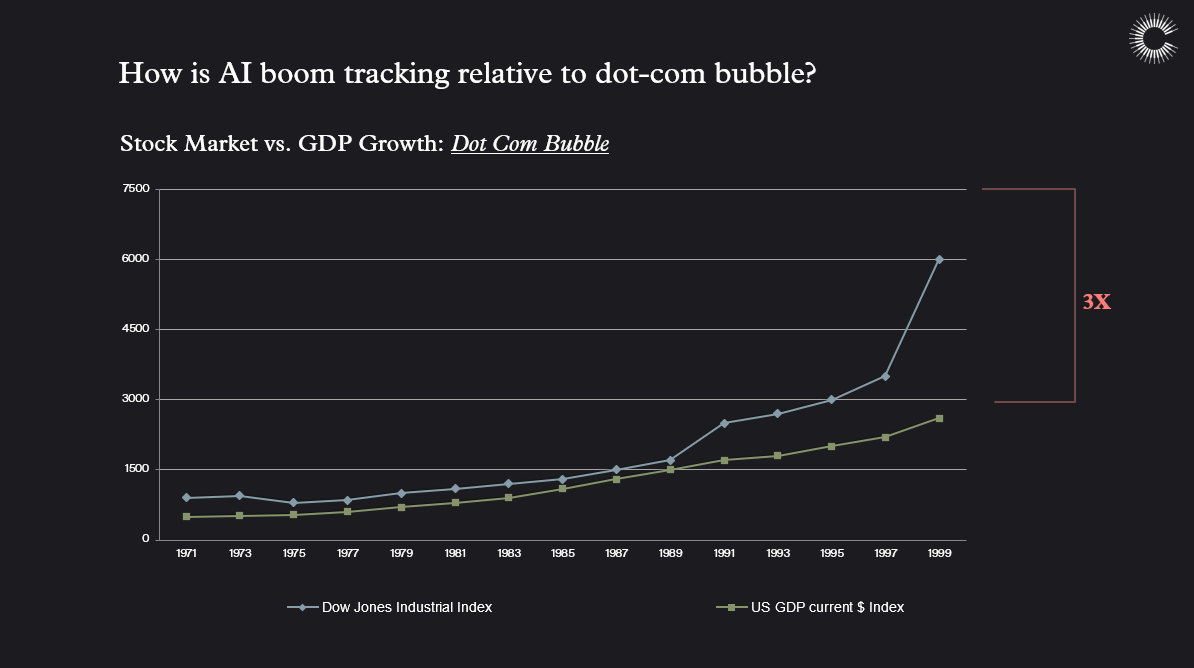

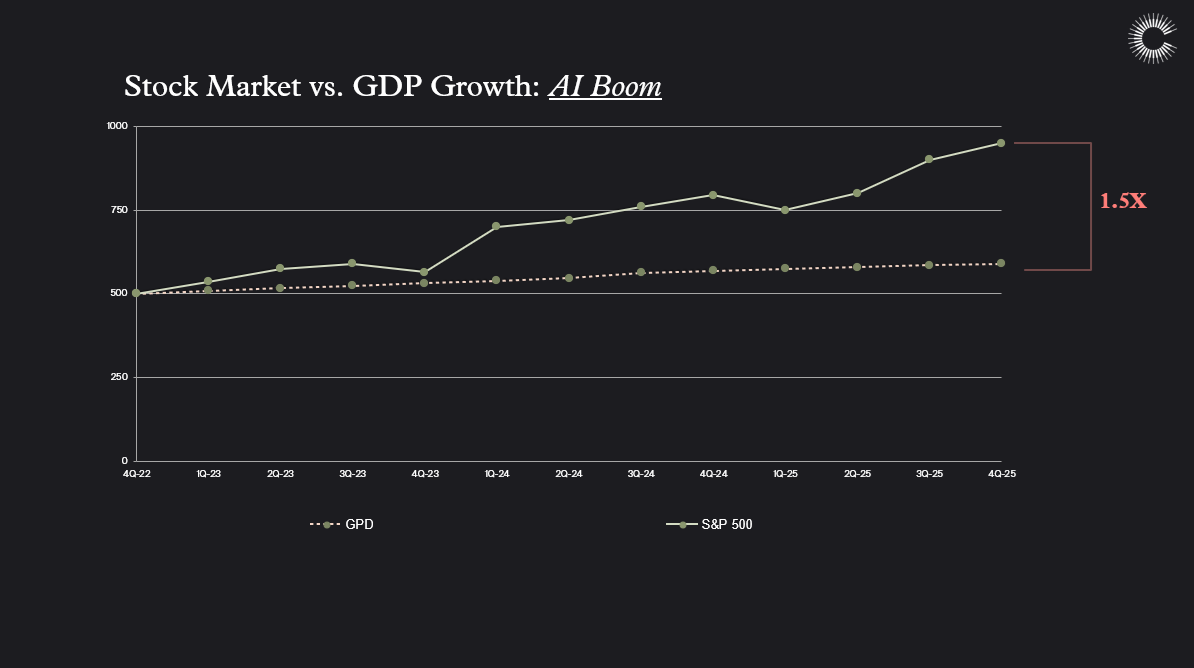

AI Is Reshaping Venture, But the Question of a Bubble Looms

AI-related deals made up 61% of all VC investments in 2025, a concentration that has no precedent in recent venture history. Total AI-related VC investment has surged well past $200 billion annually, dwarfing the levels seen even during the 2020-2021 boom.

A recurrent question is whether this resembles a bubble. During the dot-com era, the stock market ran roughly 3x ahead of GDP growth before the correction hit. In the current AI boom, the S&P 500 has outpaced GDP by about 1.5x. That gap is narrower, but the trend bears watching. If the market continues to run ahead of economic output without corresponding revenue growth from AI deployments, the risk of a correction increases.

At Deep Tech Week, Nic noted that 2026 may be the year the real economy starts pulling AI expectations back down to earth. The question is not whether AI is transformational, but instead whether the capital being deployed today will generate returns commensurate with the valuations being assigned.

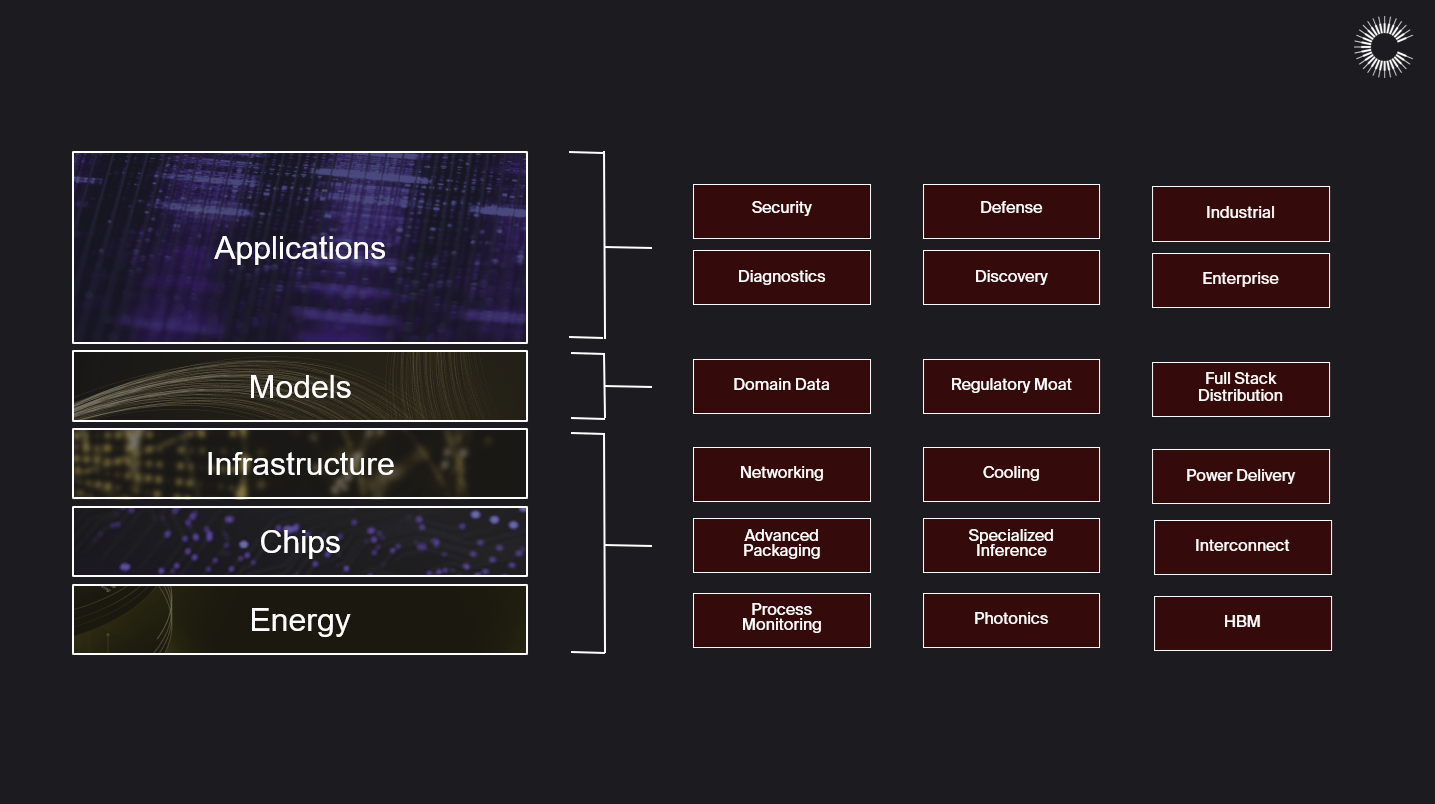

Where the Opportunities Are in the AI Stack

We see distinct opportunities for startups throughout every layer of the AI stack.

At the energy and chip-level companies are tackling cooling, power delivery, photonics, advanced packaging, and high-bandwidth memory. These are capital-intensive businesses but are also where some of the deepest moats are being built. The constraints on AI scaling today are increasingly physical.

At the infrastructure and model layers, networking, specialized inference hardware, and process monitoring are all areas where startups can carve out defensible positions. At the application layer, the strongest companies tend to have some combination of domain-specific data, regulatory moats, or full-stack distribution that insulates them from commoditization.

The key message from our panel: founders should resist the temptation to chase the model layer, where competition is fierce and margins are under pressure. The better opportunities often sit lower, where the technical barriers are higher, but there is still opportunity to build durable competitive advantage and customer relationships are stickier.

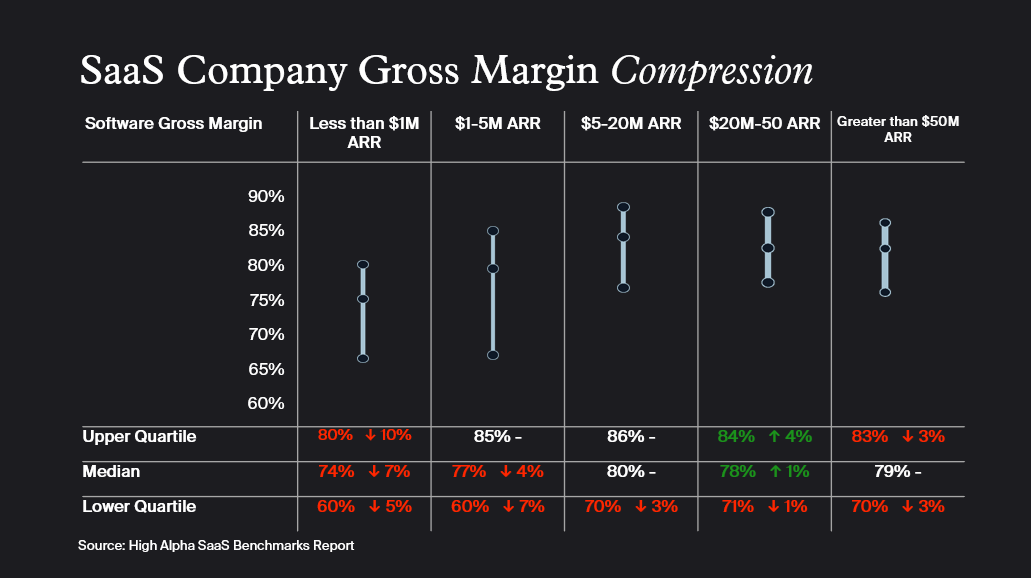

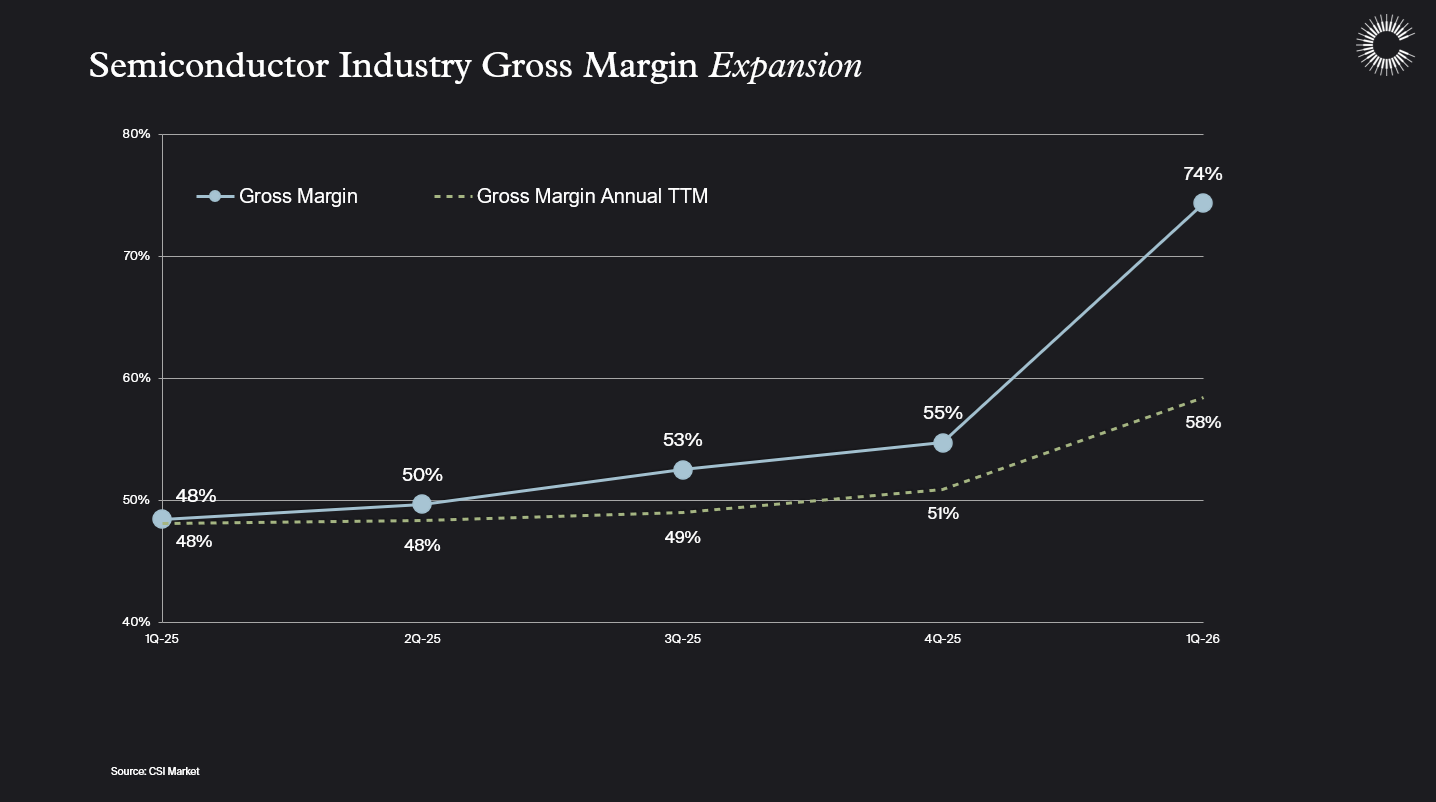

The Software-Hardware Margin Flip Is Real

One of the most significant structural shifts underway is the inversion of margin dynamics between software and hardware. SaaS company gross margins are seeing compression across every ARR tier. AI compute costs embedded in software products are a major driver.

Meanwhile, the semiconductor industry has seen gross margins expand from more than 25% between early 2025 and Q1 2026. That is a remarkable move in a short period, driven by pricing power in AI-related chips and growing demand for specialized hardware.

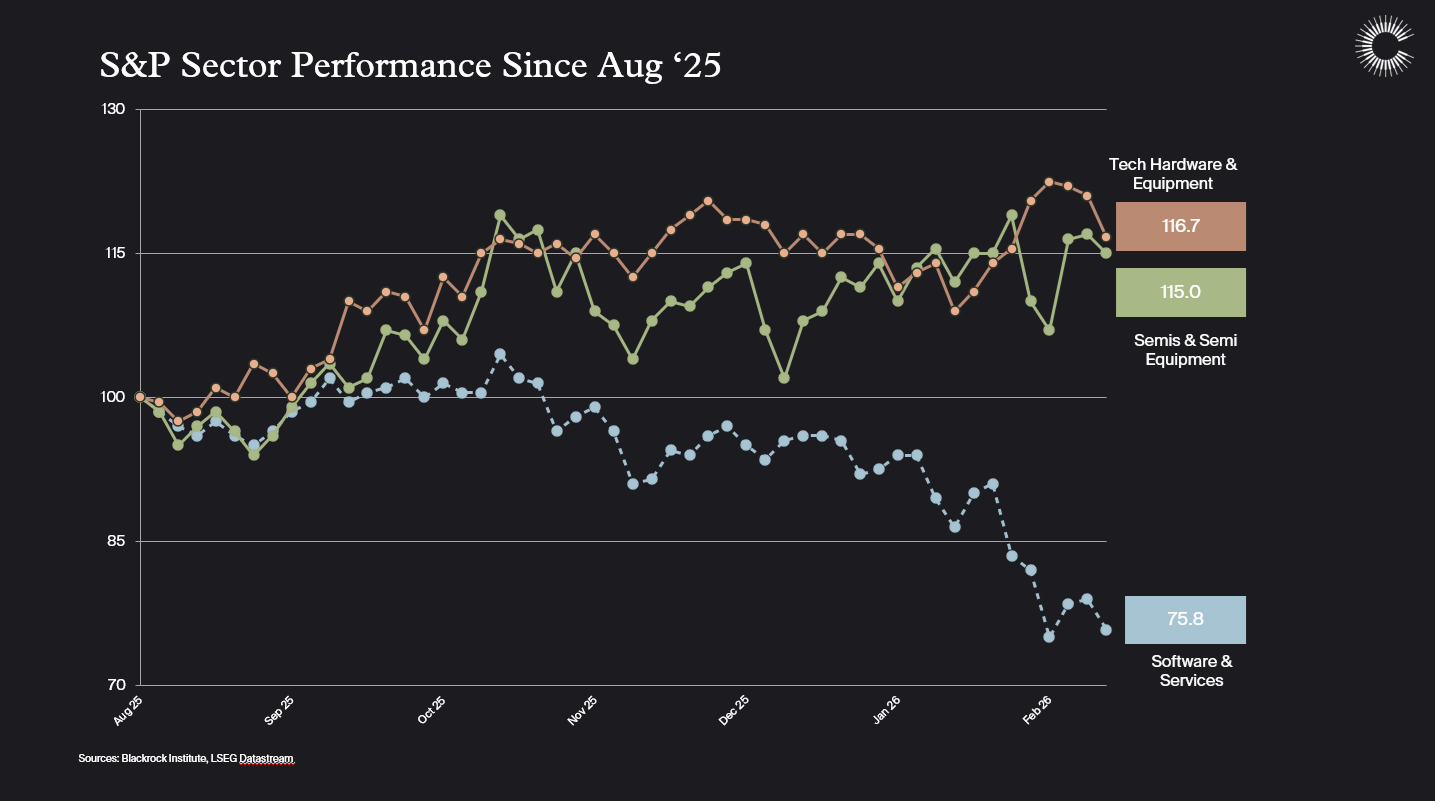

S&P sector performance data tells the same story via the public markets. Since August 2025, tech hardware and equipment is up 16.7%, semiconductors are up 15%, and software and services are down more than 24%. The market is repricing these sectors in real time.

Michael Marks made this point directly at the event: “For years, the venture world treated hardware as a worse business than software. That framing has always been wrong and is totally out of date thinking today. Startups with real hardware IP and pricing power are building durable, high-margin businesses”.

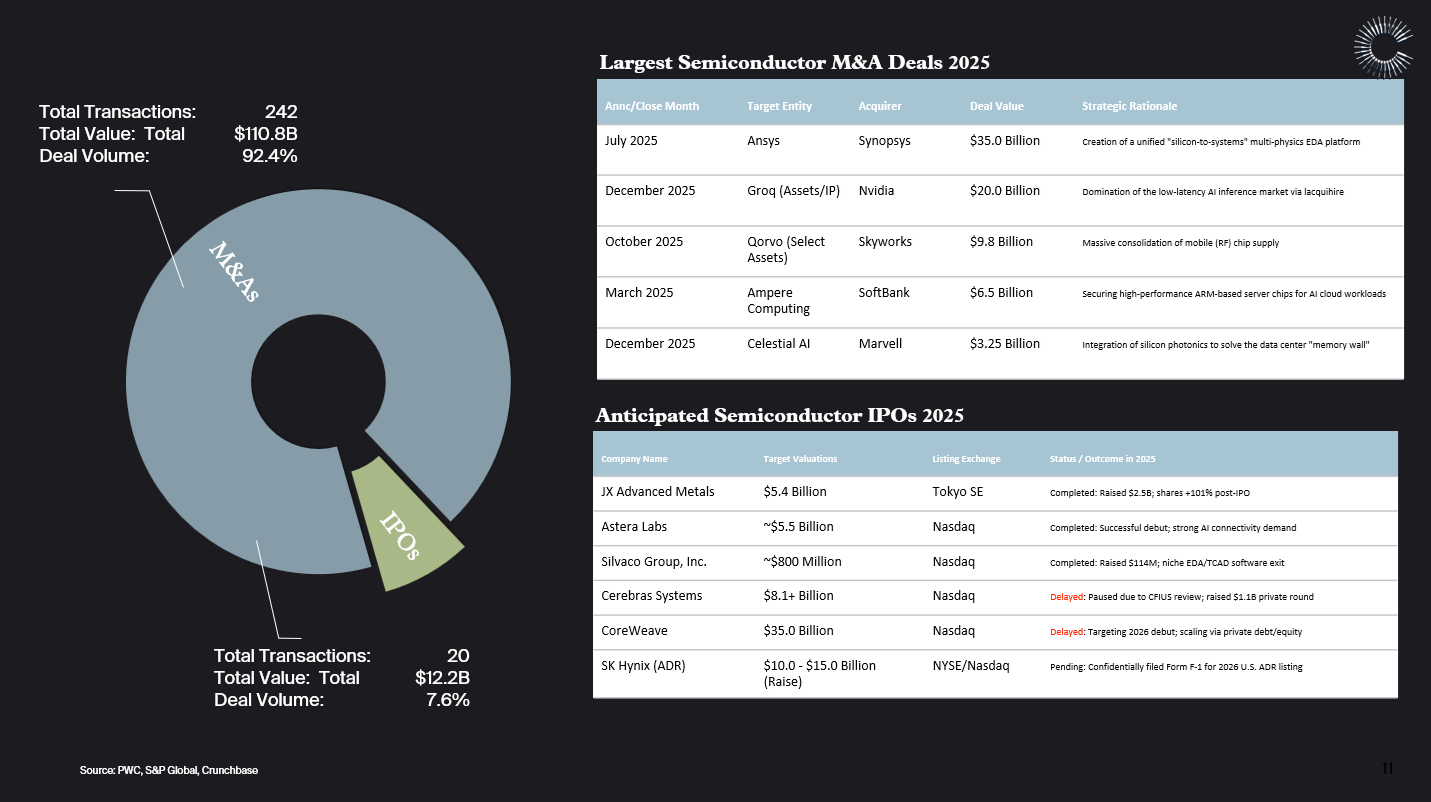

Semiconductor Exits: M&A Dominates, IPO Window Is Selective

In 2025, the semiconductor exit landscape was dominated by M&A. The largest deals reflect strategic consolidation: Synopsys acquired Ansys for $35 billion to build a unified EDA platform, Nvidia picked up Groq assets for $20 billion to lock down low-latency inference, and Skyworks consolidated mobile RF chip supply by acquiring select Qorvo assets for $9.8 billion.

The IPO window has been more selective. JX Advanced Metals and Astera Labs completed successful listings, but Cerebras Systems paused its IPO due to CFIUS review and CoreWeave pushed its debut to 2026. The takeaway for founders is that M&A remains the more reliable exit path in semiconductors, and the acquirers are paying meaningful premiums for companies with differentiated technology.

The Groq outcome, discussed at length during the panel, raises an interesting strategic question. Does a $20 billion acquisition by Nvidia validate the thesis that startups can challenge Nvidia in AI inference, or does it prove that the most likely endgame is absorption by the incumbents? The answer is still very much up for debate and depends significantly on whether a startup is focusing on the training or inference market.

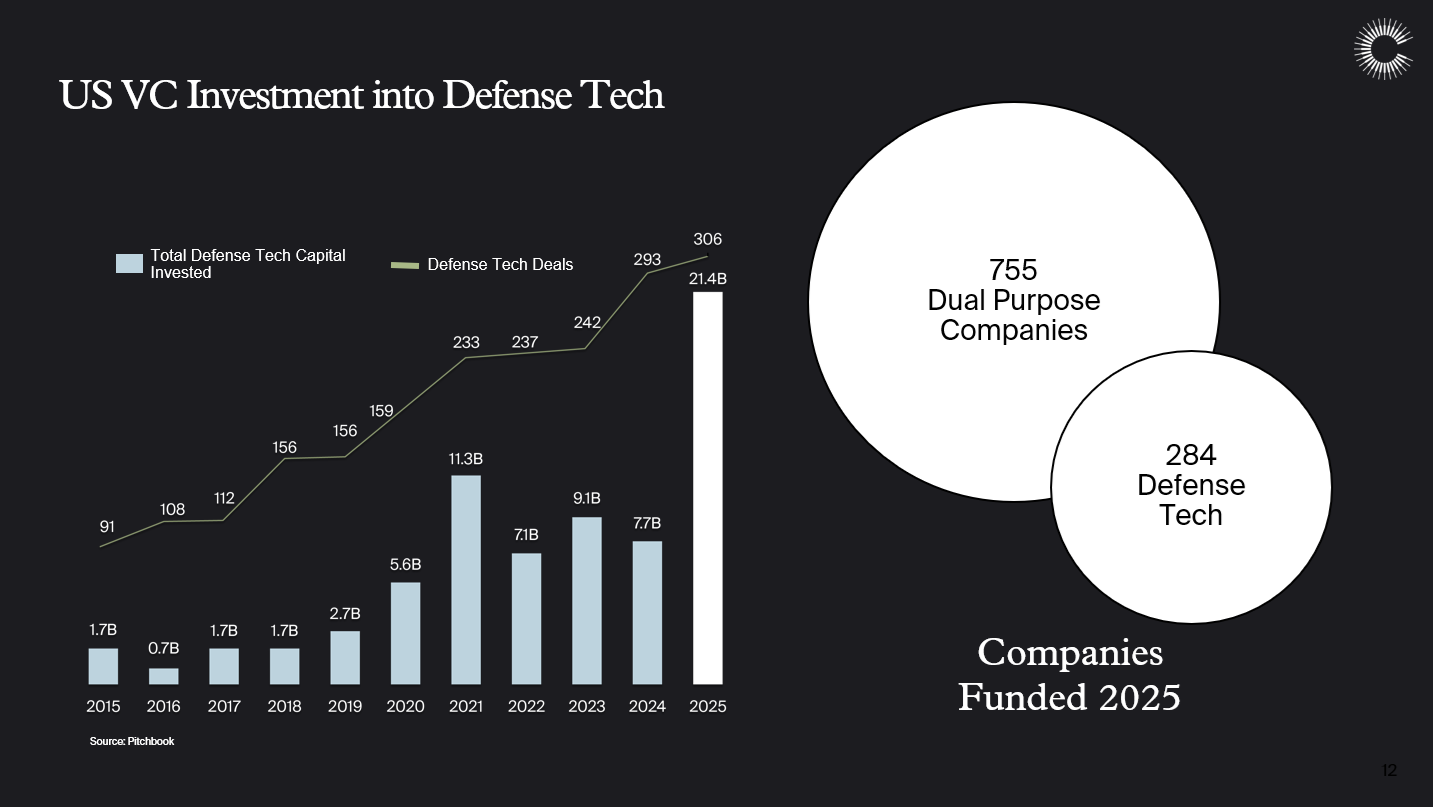

Defense Tech Is No Longer a Niche

U.S. VC investment in defense tech reached $21.4 billion in 2025, spread across 306 deals. That is nearly triple the $7.7 billion invested just two years earlier. The number of funded companies tells a similar story: 755 dual-purpose companies and 284 pure defense tech startups received funding in 2025.

The growth trajectory has been steady since 2015, when total defense tech capital was just $1.7 billion across 91 deals. What changed is a convergence of factors: rising global military spending, bipartisan political support for defense modernization, and the recognition that commercial AI and autonomy technologies have direct national security applications.

Michael Marks emphasized during the discussion that while it may be hyped up today, defense is still a challenging space for most investors. The most investable defense tech companies are those building technology that serves both commercial and government customers. Dual-use models create larger addressable markets, diversify revenue risk, and avoid the long procurement cycles that have historically made defense a difficult category for venture.

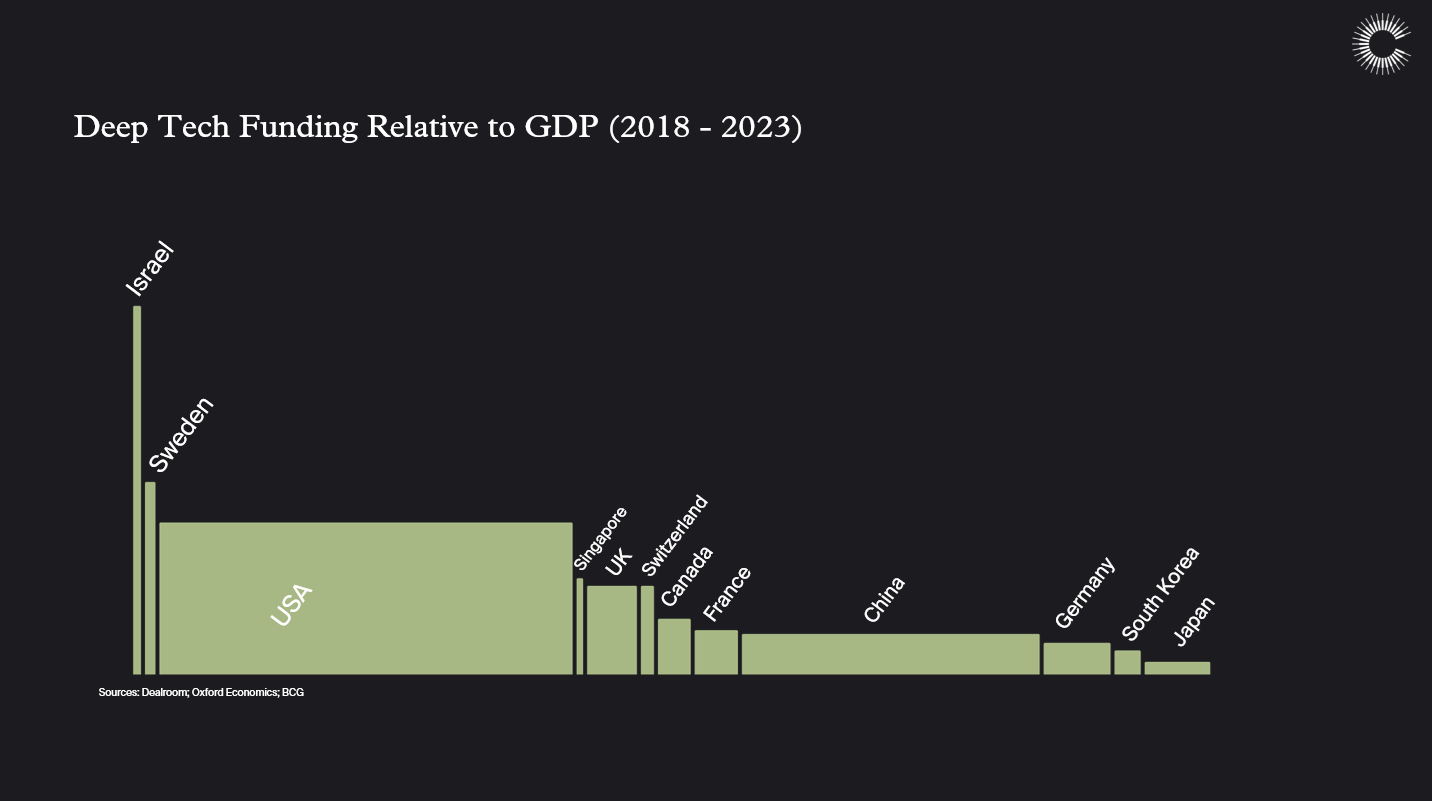

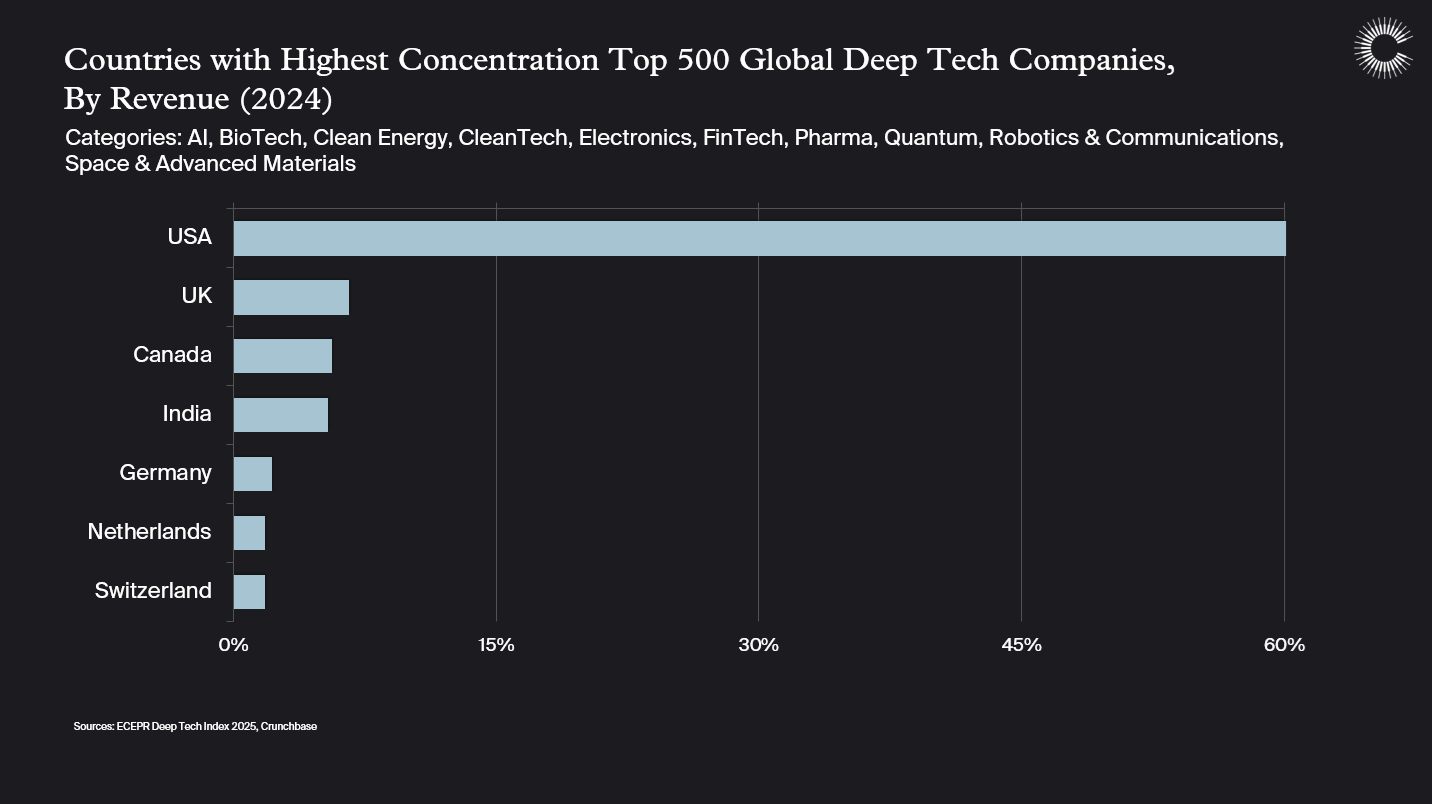

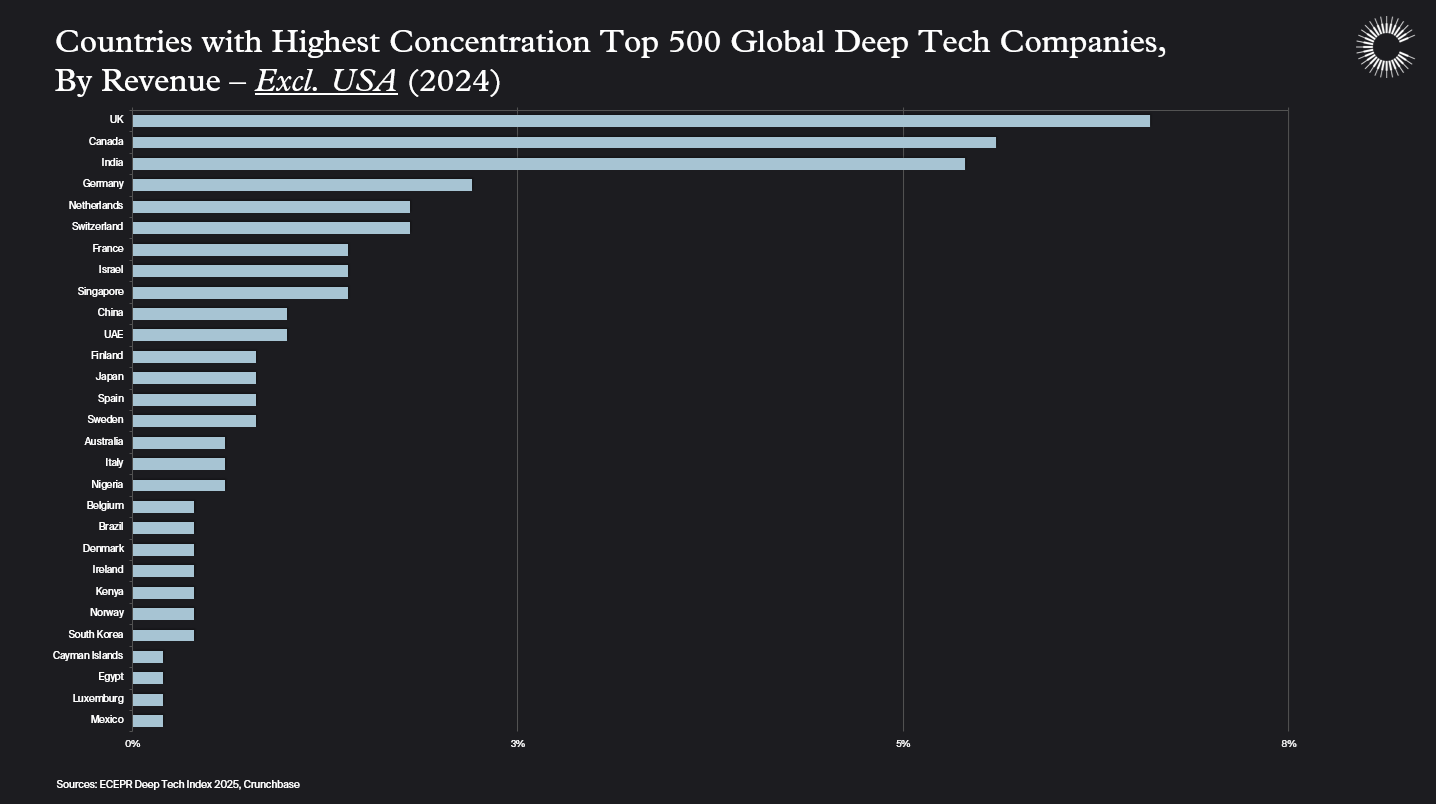

The U.S. Still Dominates Deep Tech, But New Hubs are Rising

The U.S. accounts for the largest share of the top 500 global deep tech companies by revenue, but the distribution outside the U.S. is notably broad. The UK, Canada, and India each have meaningful concentrations, followed by Germany, the Netherlands, Switzerland, France, and Israel.

When measured by deep tech funding relative to GDP, Israel and Sweden lead by a significant margin, followed by Singapore, the UK, and Switzerland. The U.S. remains dominant in absolute terms but is not the leader on an intensity basis.

Celesta invests globally, with portfolio companies in Israel, India, Canada, Japan, China, and the U.S. As Nic noted at the event, the key indicators of a region being ready for more deep tech investment include strong university research pipelines, existing clusters of engineering talent, and crucially, the links back to Silicon Valley for talent, capital, and go-to-market support. The center of gravity has not shifted away from the Valley, but the best companies are increasingly being built in partnership across multiple hubs.

Looking Ahead

Deep tech investing is no longer an emerging category. It is a major, growing share of the global venture market, driven by structural demand for AI infrastructure, defense modernization, and hardware innovation. The data we shared at Deep Tech Week reflects a market that is maturing rapidly but still has significant room to develop.

For founders, the message is to focus on defensible technology, build toward real milestones that support valuation step-ups, and solve for access to capital rather than optimizing for the highest valuation on any single round. For investors, the opportunity is substantial, but discipline matters more than ever as valuations rise and competition for deals intensifies.

Data sources: BCG, Dealroom, Carta, Bureau of Economic Analysis, Bureau of Labor Statistics, SVB, OECD AI / Preqin, High Alpha, CSI Market, Blackrock Institute, LSEG Datastream, PWC, S&P Global, Crunchbase, Pitchbook, ECEPR Deep Tech Index, Oxford Economics.